%20(1).png)

In its Q1 2025 earnings call, Lam Research reported strong performance and emphasized growth opportunities, particularly in etch and deposition technology. CEO Tim Archer highlighted optimism for NAND spending recovery in 2025, supported by technology upgrades and a transition to molybdenum through Lam’s advanced Atomic Layer Deposition (ALD). Lam is positioned to capture opportunities in advanced semiconductor nodes like gate-all-around and EUV patterning, while its expanded offerings in high-bandwidth memory (HBM) and advanced packaging align with growing demand in AI and high-performance computing. Despite regulatory challenges in China, Lam continues to serve this market by focusing on upgrades and services. Looking ahead, Lam expects to outpace industry growth, driven by its strategic positioning across advanced technologies.

In its Q1 2025 earnings call, Lam Research Corporation (NASDAQ: LRCX) reported solid performance and reiterated optimism for growth in 2025, largely driven by demand for etch and deposition technologies. CEO Tim Archer emphasized Lam’s strategic positioning in an industry experiencing technological shifts, despite a prolonged downturn in NAND spending.

Lam anticipates a recovery in NAND spending in 2025, largely driven by technology upgrades rather than new capacity expansions. Key factors include a transition from tungsten to molybdenum in NAND structures, which improves performance by reducing resistivity. Lam is well-positioned in this area due to its extensive installed base and production wins, projecting an advantageous position as these upgrades scale into 2025.

NAND Technology Upgrades Set to Drive Etch and Deposition Demand in 2025

While the NAND segment has been in a prolonged downturn, Lam anticipates a recovery in 2025 as manufacturers upgrade to advanced nodes. The push toward 3D NAND layers exceeding 200 is essential to meet the growing demand for high-speed, high-capacity storage in data centers and client devices. Currently, about two-thirds of NAND capacity remains at older technology nodes, highlighting significant room for technology upgrades. Lam’s extensive installed base of NAND equipment positions it well to benefit as customers look to improve efficiency and performance.

Furthermore, Archer highlighted a shift from tungsten to molybdenum as a key materials change in NAND, addressing word line resistance challenges. This transition is particularly favorable for Lam, as it has already secured production wins in molybdenum deposition, which will scale up throughout 2025. These advancements are expected to enhance Lam's leadership position in NAND technology transitions.

Lam's product offerings mentioned in the reporting, along with their primary applications and strategic impacts.

Advanced Logic and Foundry Nodes: Key Growth Segments for Lam

Lam is also poised to benefit from shifts in advanced logic and foundry nodes, which are increasingly adopting gate-all-around architectures, backside power distribution, and advanced EUV patterning. These cutting-edge technologies require more intensive use of etch and deposition processes, aligning with Lam’s expertise and product offerings.

Archer noted the company's recent wins in selective etch tools and other innovations that support these advanced nodes, positioning Lam favorably as customers transition to architectures with greater power and performance needs. This expanding demand from foundry and logic customers offers a substantial growth opportunity for Lam’s advanced etch and deposition technologies.

Advanced Packaging Driven by AI Fuels Revenue Growth

The AI and high-performance computing boom has intensified demand for advanced packaging, particularly for high-bandwidth memory (HBM). Lam’s copper plating technology, SABRE 3D, has experienced substantial adoption, doubling its market share this year. This growth has been fueled by the rising complexity of 2.5D and 3D packages, which require high-performance interconnections to support AI-driven systems.

Lam anticipates this trend will continue into 2025 as the industry moves toward more advanced and intricate packaging solutions. According to Archer, advanced packaging will play a critical role in the semiconductor ecosystem for the foreseeable future, and Lam’s early investment in this technology has positioned it for continued market share gains.

Supporting Installed Base and Productivity in Memory Markets

Lam’s Customer Support Business Group (CSBG) has also shown growth, focusing on productivity enhancements and tool reuse. With Lam’s extensive tool installations in both DRAM and NAND, customers are prioritizing upgrades over entirely new systems, especially as they look to improve cost efficiency during NAND’s down cycle. This focus on tool reuse has led to recent market share gains for Lam, as existing tools are upgraded for better value than new installations.

As DRAM and NAND customers intensify efforts to reduce costs, Lam’s service-oriented model and productivity solutions, including equipment intelligence services, have seen greater adoption. This trend underscores Lam's ability to support its customers' evolving needs in an era of increased etch and deposition intensity.

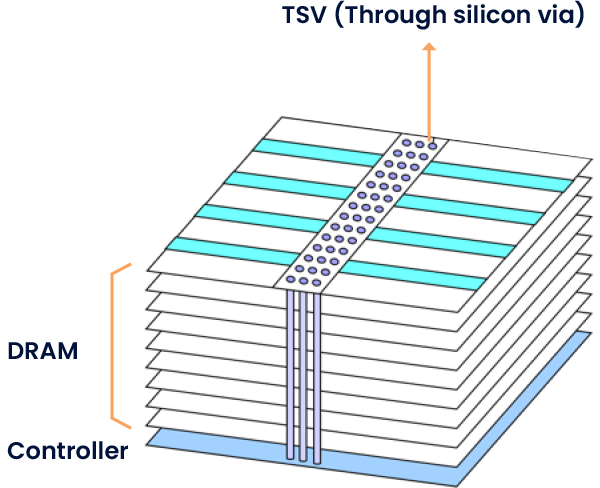

Lam Research Leverages ALD for Moly Transition in NAND, Driving Next-Gen Semiconductor Performance

Lam Research's perspective on ALD is optimistic, particularly as it becomes increasingly essential in NAND technology upgrades. The company highlighted the industry's ongoing shift from tungsten to molybdenum (moly) for improved resistivity in 3D NAND structures, a transition that Lam’s ALD technology is well-positioned to support. Lam has already secured production wins for ALD applications with molybdenum, expected to ramp up significantly in 2025. This capability extends beyond NAND, with potential applications in DRAM and advanced logic/foundry nodes, underscoring ALD’s growing importance in meeting next-generation semiconductor demands.

Lam Research Adapts to Regulatory Challenges as China Revenue Set to Decline in 2025

In its Q1 2025 earnings presentation, Lam Research highlighted key developments and expectations for the China market. China accounted for roughly 37% of Lam's revenue in the September quarter, but the company anticipates this share will decrease to around 30% by December and potentially decline further in 2025. This projected downturn reflects both anticipated shifts in demand and the impact of U.S. export restrictions on advanced semiconductor equipment sales to China. Lam acknowledged the challenges posed by ongoing and potential new U.S. export controls, which could limit its ability to sell to certain advanced technology segments in China. Nevertheless, Lam remains committed to supporting its domestic Chinese customers within the boundaries of regulatory compliance, expecting demand in restricted segments to normalize as global WFE (wafer fabrication equipment) spending adjusts.

Much of Lam's business in China now focuses on servicing domestic fabs with tools for trailing-edge and specialty node processes, areas that generally remain unaffected by export controls. Through its Reliant product line, Lam continues to support these nodes, emphasizing upgrades and maintenance services as primary offerings in a market constrained by new advanced technology sales. Despite potential reductions in advanced equipment sales, the company is confident that its service and support model will help stabilize revenue in the region. By prioritizing productivity solutions and customer support, Lam is adapting to a complex regulatory environment while anticipating that China’s share of its revenue will gradually normalize amid a broader decline in WFE spending in the country.

Strategic Positioning in 2025 and Beyond

In summary, Lam Research is set to capitalize on a growing demand for etch and deposition technology driven by the industry’s shift to advanced architectures. Archer concluded the call with optimism, stating that the company is well-positioned to capture market share as the semiconductor industry increasingly relies on complex, three-dimensional structures. With its advanced product offerings, Lam expects to outperform overall wafer fabrication equipment (WFE) growth in 2025, strengthening its leadership across multiple semiconductor sectors.